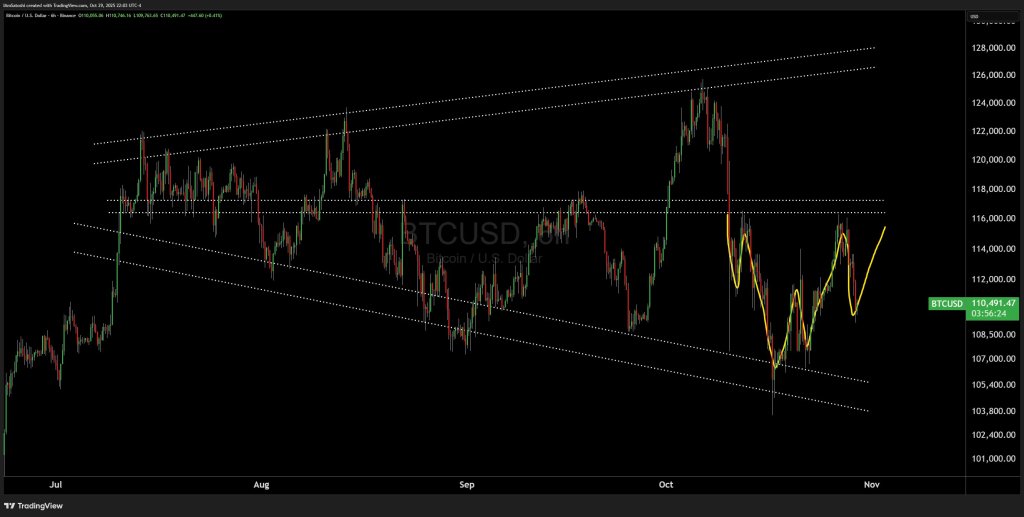

Bitcoin is sitting on a technical ledge that could decide whether price makes a new all-time high or unwinds sharply into the $80,000s, according to veteran trader Josh Olszewicz (CarpeNoctom). “BTC complex iHS brewing in the megaphone,” he posted on October 30, 2025, adding in a follow-up: “Also this brewing, not great.”

The Bullish Case For Bitcoin

Olszewicz is tracking two structures. The first, on the 6-hour timeframe, shows BTC trading inside a broadening “megaphone” pattern that has contained price since July. The megaphone is defined by rising dotted resistance lines above and falling dotted support lines below. The upper boundary extends through roughly $126,000 to $128,000. The lower boundary widens down toward $105,400 and $103,800.

Within that range, Bitcoin put in a sharp spike above $126,000 in early October, then sold off violently, dropping below $106,000s with a wick toward roughly $102,000. That bounce failed to recover the prior range. Instead, price stalled under a horizontal resistance shelf around $116,000–$117,000. Olszewicz sketches a yellow projected path that implies a short-term bounce from just under $111,000 back towards $116,000. That path suggests attempted relief, not confirmed bullish continuation.

Only if Bitcoin can reclaim the $116,000–$117,000 zone does a move toward the upper resistance band come back into play. In that scenario, price could extend toward $128,000, print a new all-time high, and potentially restart a broader recovery phase.

The Bearish Case For Bitcoin

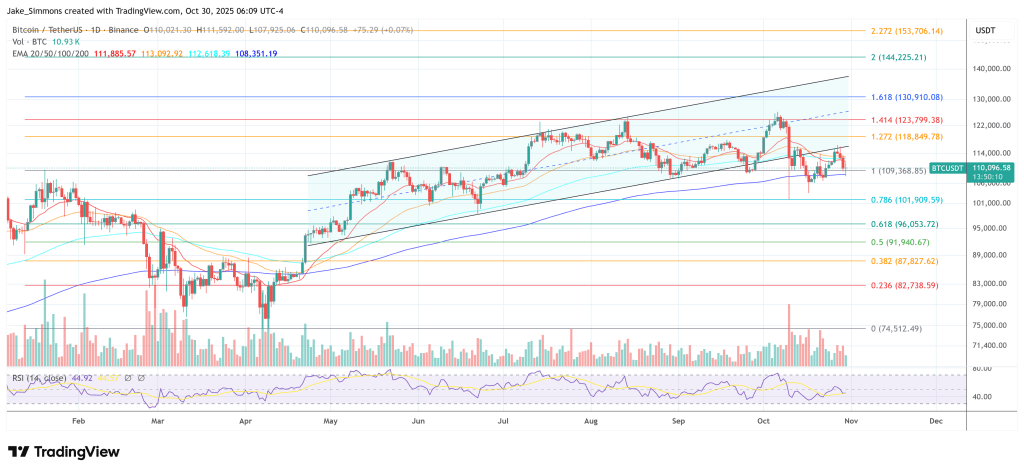

The second chart is where the downside risk accelerates. On the 1-day timeframe, Olszewicz maps a head-and-shoulders top with a rising neckline. The left shoulder topped in the $118,000 area, the head reached roughly $126,200, and the right shoulder again failed near $116,000. The neckline is drawn as an ascending dotted support line that now sits in the $105,000–$106,000 zone. He highlights $107,316.81 as the key breakdown level.

If that neckline breaks decisively, the chart applies a standard measured move. The distance from the head down to the neckline is projected lower. Olszewicz plots that extension into a teal target zone and marks intermediate and full objectives at $93,963.81 (the 1.618 extension) and $87,652.27 (the 2.0 extension). In other words, a clean daily breakdown through $107,316 opens a path first toward the mid-$90,000s and then toward roughly $87,600.

Above spot, resistance remains layered. The 0.5 retracement of the prior impulse is labeled at $115,486, and the 1.0 retracement — effectively the previous swing high — is marked at $124,477.

Structurally, Bitcoin is now boxed between supply in the $116,000 region and that neckline supports around $105,000–$106,000. Olszewicz’s message is that bulls may still be trying to form a “complex inverse head-and-shoulders in the megaphone,” but the active daily head-and-shoulders top is “not great.” A decisive loss of the neckline could confirm the bearish structure and put $93,963.81 and $87,652.27 on the table.

In a post on X on October 29, Quinn Thompson, CIO of Lekker Capital, argued that Jerome Powell’s post-FOMC messaging was less about macro uncertainty and more about pressure tactics aimed at the political apparatus — with direct consequences for crypto liquidity.

Powell’s FOMC Comments Decoded

Thompson wrote: “Powell appeared to be playing political games / posturing / CYA around the December verbiage, possibly to communicate to the admin to get the government reopened. It almost felt like a threat that if no data (due to continued government shutdown), then there won’t be a December cut and the market was briefly thrown off by that uncertainty.” He called out how abnormal it was to hear Powell comment this directly on market expectations: “The immediate reaction made sense given it is quite abnormal to hear Powell comment on market pricing so specifically as he always refrains from doing so and makes a point to say he will not comment on market pricing.”

That is the core of Thompson’s read. Powell just broke his own habit. Powell tends to reject any framing that implies the Fed is validating market forward pricing. This time, after the Federal Reserve cut its policy rate by 25 basis points to a target range of 3.75%–4.00%, Powell said explicitly that “a further reduction in the policy rate at the December meeting is not a foregone conclusion — far from it.”

He underlined that there are “strongly different views” inside the Committee about the speed and depth of further easing. Markets immediately repriced. Treasury yields moved higher and the probability of a December cut fell sharply from near certainty to something closer to a coin flip, and risk assets reacted accordingly. That includes crypto: bitcoin and large-cap crypto assets initially traded lower alongside equities as the market read the comment as a hawkish surprise rather than as positioning.

Thompson’s view is that this was not about signaling a hawkish turn. It was about signaling conditionality. He frames Powell’s remarks as a message to the White House and Congress: reopen the government, restore economic data flow, and the Fed has cover to cut again in December; keep the shutdown in place and deny the Fed official data, and Powell can say, on record, that he cannot justify further accommodation. Powell himself emphasized that the central bank has been operating “in the absence of key government data” because the shutdown that began on October 1 has blocked normal labor, inflation, and activity reporting. Thompson characterizes that stance as an implicit warning shot.

In his words, “What you infer from that is up to you, but additionally I believe the market may have been surprised by what I believe to be an incorrect Fed reaction function to the government shutdown. There is no scenario in which the economy is stronger because of the shutdown and if they are highlighting continued downside labor market risks, there isn’t a great case to be made to veer from their September dot plot path.”

For crypto, the subtext is important: Thompson is saying Powell’s comments were not a signal to tighten financial conditions into year-end. They were leverage in a political negotiation, not a policy ceiling on liquidity.

That point is operational, not rhetorical. Thompson is saying the Fed’s stated logic does not actually line up with what the Fed itself claims to be worried about. Powell’s justification for the October 29 cut leaned heavily on labor market softening and downside employment risk. The official FOMC statement pointed to a “shift in the balance of risks” toward weaker employment, noted that job gains have slowed, and acknowledged that unemployment has edged higher.

Powell also said inflation is still above target but no longer accelerating the way it was earlier in the year, which is why some members favored faster easing. That mix — weakening labor, cooling inflation, policy cuts — has historically been constructive for crypto because it points to easier dollar liquidity and a lower cost of capital without outright crisis.

On the balance sheet, Thompson highlights something that is already documented in Fed and press statements but has not yet fully repriced across risk: “Just a week or two ago the market was not expecting QT to end this soon and today Powell went so far as to discuss the next step in this process being a return to balance sheet growth. These developments are definitively liquidity positive, even though the MBS reinvestment and future purchases will be all or predominantly bills.”

What This Means For Crypto

In plain terms, the Fed didn’t just cut rates by 25 bps. It also said it will stop quantitative tightening on December 1. That means the Fed will no longer allow its Treasury and mortgage holdings to roll off passively. Instead, it will reinvest maturing Treasuries back into Treasuries and redirect principal paydowns from its mortgage-backed securities portfolio into Treasury bills.

For crypto, this is the line that matters. When the Fed stops shrinking its balance sheet and starts recycling back into bills, it’s effectively injecting incremental dollar liquidity into the system, even if it refuses to call it QE. That liquidity has historically leaked into the parts of the market most sensitive to excess cash and duration scarcity — tech, high beta credit, and crypto. Thompson is basically saying that under the surface of Powell’s cautious language, the Fed just signaled the start of the next crypto liquidity regime.

This is a critical liquidity inflection that is easy to miss if the only headline you absorb is “December cut not guaranteed.” Ending QT this early was not a consensus two weeks ago. This is also why Thompson rejects the idea that Powell’s tone was structurally bearish for risk.

He writes, “All in all I think the December cut is still quite likely.” He then lays out the macro sequence he expects to see once the shutdown ends: “Ultimately I think they will reopen the government in the next few weeks so there will be data and it is likely to show inflation falling for the next few months and labor market continue its weakening path, and Trump is making deals that likely bring tariffs down which also earns him brownie points with the FOMC.” The message for crypto investors is that once data resumes, it will justify continued easing, not block it.

The last part of Thompson’s post moves from mechanics to governance. He points directly at Powell’s expiring authority. “Powell’s term as Chair ends in 6 months and his successor will be known even sooner, creating a shadow Fed chair situation. It remains clear to everyone and the market that the new chair will be friendly towards and help effectuate the admin’s agenda. Given all of the above, it is difficult for me to paint a risk asset bear case based upon liquidity dynamics as all signs point to continued massaging to support markets.” That is the crypto punchline.

Thompson is arguing that the institutional bias of the Fed, going into the succession window, is toward maintaining and managing liquidity conditions so markets do not crack. If that bias holds, it is inherently crypto-bullish, because it implies a policy floor under dollar liquidity at the exact moment the Fed is already preparing to halt balance sheet runoff and re-expand via bills.

At press time, the total crypto market cap stood at $3.73 trillion.

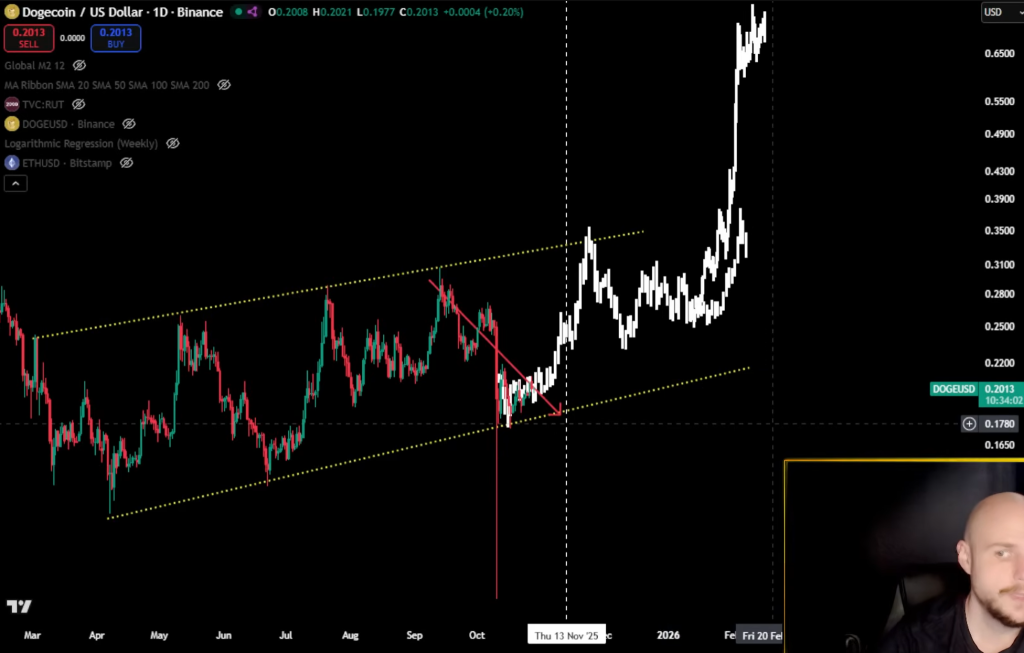

Crypto analyst VisionPulsed argues that Dogecoin is entering a seasonal window of strength in November—conditional on a broader “risk-on” handoff from US equities to crypto and, critically, Bitcoin maintaining support at a key moving average. In an Oct. 28 video update focused on Dogecoin, he linked the coin’s near-term upside to a now-familiar sequence: S&P strength → Russell 2000 catch-up → Ethereum breakout → DOGE momentum.

“November could be repeating itself where we get a big push in November,” he said, citing what he frames as a recurring pattern of late-October bottoms followed by November reversals in recent years. He pointed to 2022 and 2023 as examples and opened the session by noting ongoing equity optimism, quipping that “the S&P is continuing to gap up,” and that a risk-bid in stocks historically creates favorable conditions for crypto beta.

November Preview For Dogecoin

The pathway he sketches is explicit and hierarchical. “If the S&P can push higher, then the Russell 2000 may actually follow… And as we’ve said 100 times, when the Russell breaks out, that increases the chance that Ethereum breaks out. Happened in 2017, happened in 2020. And if the Russell can break out and Ethereum can break out, slap Dogecoin on there.” His Dogecoin view is framed inside a rising channel, with price “grinding upwards on the trend line” into early November before a potential acceleration toward the channel top in mid-month.

The analyst is emphatic that the setup is constructive but not a done deal. “There’s probably no big bull run just yet, but it looks bullish from here to at least December.” From there, the branching outcomes hinge on whether an altseason materializes and whether DOGE can break beyond the upper boundary of its channel.

If momentum stalls at resistance without evidence of declining Bitcoin dominance—his shorthand for capital rotating into altcoins—he warns of a familiar whipsaw: “If we come up to the top of the channel and we get stuck again… we’re going to see a crash to the bottom of the channel or at least the middle.”

In that downside branch, he cites a drawdown scenario toward the low-teens, saying DOGE could “go back to 13 cents.” In the upside branch, if an altseason ignites, he floats a run toward “80 cents, 90 cents, whatever,” with the caveat that such a surge into December could also mark a local cycle top requiring reassessment in real time.

As a gating condition across all scenarios, Bitcoin’s trend integrity remains the fulcrum. “If for whatever reason, Bitcoin breaks this moving average, then there’s no bull run at all. It doesn’t exist—we’re in a bear market. But as long as we hold a moving average… the bull run will continue.”

He analogizes the dynamic to a “blue circle” bounce on the S&P and expects a comparable moving-average response from BTC to keep the crypto risk cycle intact. The Ethereum leg is treated as both a beneficiary of small-cap equity strength and a validator for alt rotation: “If the S&P and the Russell can both push higher, that gives us a green light for Ethereum. And if Ethereum can push higher, then Doge could push higher.”

Timing is central to his thesis. He anticipates a steady “grind” into early November, a push toward DOGE’s channel top “probably in the middle of November,” and then a decisive inflection as the market either confirms altseason into December—or fails and resets with one more flush before any sustained rotation. He also leaves room for a less popular possibility: “We always have to keep our open mind to the possibility that there is no altseason… I’m the last person that wants to say that… but we’ve got to be open to the possibilities.”

VisionPulsed characterizes the current moment as tactically bullish with binary edges defined by the channel and BTC’s moving average. “I would say the top of the channel is in play as long as we hold the bottom of the channel.” The message to Dogecoin traders is ultimately conditional and sequence-driven: November offers the opening, but equities, Bitcoin trend support, and an Ethereum confirmation are the levers that must all click into place to turn an encouraging drift into a decisive breakout. As he signed off: “As always, none of this is financial advice.”

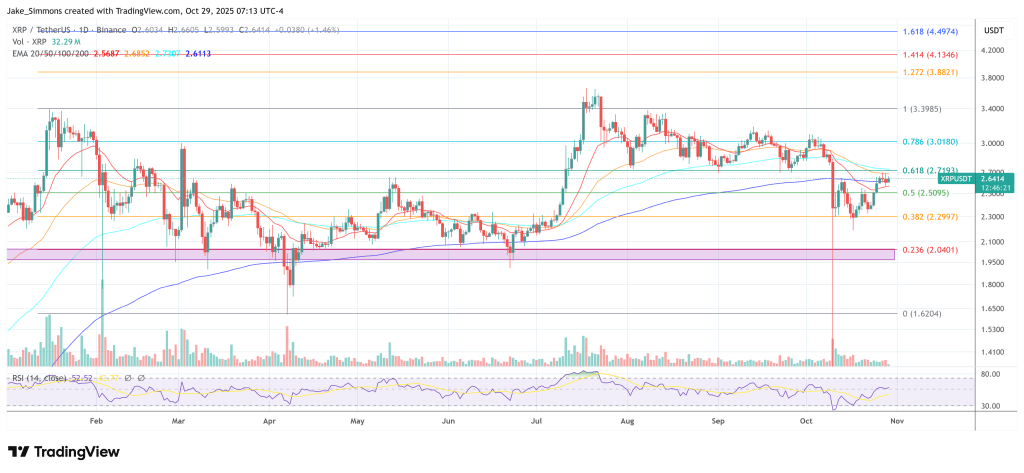

Crypto analyst Ali Martinez has cautioned that XRP may be approaching another downswing after the Tom DeMark (TD) Sequential flashed a fresh sell signal on the daily timeframe. In a new video and transcript shared alongside a TradingView chart of the Binance XRP/USDT perpetual contract, Martinez said, “XRP could be bound for a correction. The TD Sequential Indicator on the daily chart has been remarkably accurate in calling XRP’s trend reversals over the past three months, and it has just flashed another sell signal.”

Is XRP Poised For A 16%+ Drawdown?

Martinez anchored the call in a sequence of recent TD prints that he argues lined up with notable reversals. “On July 22nd, a sell signal resulted in a 24% correction. On August 8th, a sell signal led to a 17% pullback. On August 23rd, a sell signal resulted in a 13% drop. On September 15th, another sell signal preceded a 13% dip. On September 27th, a buy signal resulted in a 12% rebound. On October 22nd, a buy signal led to a 14% surge. Now, the TD Sequential Indicator just flashed a sell signal, suggesting that a pullback may be underway.”

The above chart depicts the daily candles for the XRP/USDT perpetual on Binance with TD markers annotated at the cited swing points. It shows drawdowns and rebounds close to the magnitudes Martinez lists, with boxes highlighting approximate moves of about −23.9%, −17.75%, −12.34% and −12.89% following earlier sell counts, and rebounds of roughly +12.26% and +14.25% after the late-September and late-October buy signals.

The latest candle is labeled with a new “9” sell tag near the $2.64 area shown on the chart, underscoring the analyst’s warning that the next impulse could skew lower if the pattern persists.

TD Sequential signals are timing tools, not directional guarantees, and their effectiveness is typically judged ex-post by how consistently they appear near exhaustion points. Martinez’s argument is empirical and narrowly scoped to the recent three-month sample visible on his chart, where the recorded signals coincided with local peaks and troughs to a notable degree.

The present setup therefore pivots on whether XRP respects the latest sell print as it did in July, August, and mid-September, or whether the market breaks that cadence as it occasionally does in trending environments.

Martinez is not projecting targets or durations beyond the historical analogues he enumerates, and the only explicit inference he draws is that another corrective phase is statistically plausible given the recent behavior of the TD signals on the daily chart. Based on the four most recent TD sell signals (−24%, −17%, −13%, −13%), the average drawdown is ~16.75%, which—applied to the chart’s current price around $2.64—would imply potential downside toward roughly $2.20 if the pattern repeats.

Wintermute, one of crypto’s largest market makers, struck an overtly risk-on tone in a Monday market update on X, arguing that a dovish macro turn and thawing US–China tensions have reset positioning and liquidity into a friendlier Q4 regime. In a post dated October 28, the firm wrote that “risk appetite is returning as softer CPI data and improving Trump-Xi relations lifted markets, with yields easing and volatility declining,” adding that “Bitcoin reclaimed $115k on ETF inflows and short squeezes, while DeFi and AI sectors led the recovery.”

Wintermute’s Bullish Crypto Outlook For Q4

The desk framed the impulse as both macro- and microstructure-driven. On the macro side, Wintermute pointed to “a softer US CPI print (3.0% YoY vs 3.1% expected)” and “the announcement of a Trump-Xi summit in Seoul,” which it said catalyzed “a broad rebound across assets” as the S&P 500 gained 1.9%, the VIX hovered “around 16,” and Treasury yields eased with rate-cut odds firming into this week’s Federal Reserve meeting.

On the crypto side, the update said “Bitcoin performed well with a 5.3% gain, climbing above $115k… amplified by $160m in short liquidations,” while “Ethereum tracked higher toward $4,200,” and “gold unwound nearly 7% from its highs, signaling a rotation from defensive assets into risk assets.”

Wintermute characterized the advance as broadening beneath the surface. “DeFi and AI names led gains on strong protocol revenue prints and improving on-chain activity,” while “Utilities and Tooling benefited from infrastructure-related rotation as new L2 deployments and restaking primitives drew liquidity.”

Derivatives posture turned supportive, too: “On the perp side, funding rates turned positive again across most majors… though positioning remains far from crowded.” The firm also flagged a turn in base money for crypto beta: “Stablecoin supply is ticking higher for the first time since September, reinforcing that macro tailwinds are beginning to translate into fresh inflows.

Spot demand from US spot ETFs, according to Wintermute, continues to anchor the structure even as activity cooled. “US spot BTC ETFs absorbed moderate inflows through the week even as volumes thinned, underscoring sticky structural demand.” Meanwhile, derivatives leverage “is rebuilding at a measured pace after the early-month flush,” which the firm framed as healthier—“cleaner leverage and more balanced funding.”

The house view into November is unambiguously constructive and leans on seasonality and positioning. One passage distilled the stance: “While Uptober had a bit of a false start, macro tailwinds, cooling inflation, ‘stabilizing’ geopolitical tension and a dovish FED are setting the stage for a supportive rest of the year, which historically (Q4) has been the strongest for Bitcoin.”

In its closing summary, Wintermute reiterated that “positioning is cleaner, volatility subdued, and capital rotation is gradually steering toward crypto. With liquidity conditions improving and sentiment stabilising, the setup into Q4 remains constructive, favouring further risk-on continuation.”

A Decisive Week For Crypto

The note drew immediate amplification from market commentators. DeFi analyst Ignas compressed the message into a trading takeaway: “Wintermute is telling you to max bid,” citing “yields… easing, volatility… down, and BTC reclaimed 115k helped by ETF inflows and short squeezes.” He highlighted Wintermute’s own line that “macro tailwinds, cooling inflation, ‘stabilizing’ geopolitical tension and a dovish FED are setting the stage for a supportive rest of the year.”

Whether this marks an outright regime shift or a tactically favorable window will hinge on this week’s event risk—namely the Fed decision and any concrete outcomes from the Trump–Xi engagement.

Wintermute, however, is explicit about the current state of play: markets are “rotating back into risk” with “cleaner positioning” and “calmer volatility,” Bitcoin “has reclaimed early-October losses with steady ETF inflows,” and sector leadership in DeFi and AI is consistent with an early-risk rotation. “With cleaner positioning, calmer volatility, and better macro visibility, the setup into November looks healthy for further recovery and rotation across crypto,” the firm concluded.

At press time, the total crypto market cap stood at $3.78 trillion.

Ethereum-focused treasury company ETHZilla said it has sold roughly $40 million worth of ether to fund ongoing share repurchases, a maneuver aimed at closing what it calls a “significant discount to NAV.” In a press statement on Monday, the company disclosed that since Friday, October 24, it has bought back about 600,000 common shares for approximately $12 million under a broader authorization of up to $250 million, and that it intends to continue buying while the discount persists.

ETHZilla Dumps ETH For BuyBacks

The company framed the buybacks as balance-sheet arbitrage rather than a strategic retreat from its core Ethereum exposure. “We are leveraging the strength of our balance sheet, including reducing our ETH holdings, to execute share repurchases,” chairman and CEO McAndrew Rudisill said, adding that ETH sales are being used as “cash” while common shares trade below net asset value. He argued the transactions would be immediately accretive to remaining shareholders.

ETHZilla amplified the message on X, saying it would “use its strong balance sheet to support shareholders through buybacks, reduce shares available for short borrow, [and] drive up NAV per share” and reiterating that it still holds “~$400 million of ETH” on the balance sheet and carries “no net debt.” The company also cited “recent, concentrated short selling” as a factor keeping the stock under pressure.

The market-structure logic is straightforward: when a digital-asset treasury trades below the value of its coin holdings and cash, buying back stock with “coin-cash” can, in theory, collapse the discount and lift NAV per share. But the optics are contentious inside crypto because the mechanism requires selling the underlying asset—here, ETH—to purchase equity, potentially weakening the very treasury backing that investors originally sought.

Death Spiral Incoming?

Popular crypto trader SalsaTekila (@SalsaTekila) commented on X: “This is extremely bearish, especially if it invites similar behavior. ETH treasuries are not Saylor; they haven’t shown diamond-hand will. If treasury companies start dumping the coin to buy shares, it’s a death spiral setup.”

Skeptics also zeroed in on funding choices. “I am mostly curious why the company chose to sell ETH and not use the $569m in cash they had on the balance sheet last month,” another analyst Dan Smith wrote, noting ETHZilla had just said it still holds about $400 million of ETH and thus didn’t deploy it on fresh ETH accumulation. “Why not just use cash?” The question cuts to the core of treasury signaling: using ETH as a liquidity reservoir to defend a discounted equity can be read as rational capital allocation, or as capitulation that undermines the ETH-as-reserve narrative.

Beyond the buyback, a retail-driven storyline has rapidly formed around the stock. Business Insider reported that Dimitri Semenikhin—who recently became the face of the Beyond Meat surge—has targeted ETHZilla, saying he purchased roughly 2% of the company at what he views as a 50% discount to modified NAV. He has argued that the market is misreading ETHZilla’s balance sheet because it still reflects legacy biotech results rather than the current digital-asset treasury model.

The same report cites liquid holdings on the order of 102,300 ETH and roughly $560 million in cash, translating to about $62 per share in liquid assets, and calls out a 1-for-10 reverse split on October 15 that, in his view, muddied the optics for retail. Semenikhin flagged November 13 as a potential catalyst if results show the pivot to ETH generating profits.

The company’s own messaging emphasizes the discount-to-NAV lens rather than a change in strategy. ETHZilla told investors it would keep buying while the stock trades below asset value and highlighted a goal of shrinking lendable supply to blunt short-selling pressure.

For Ethereum markets, the immediate flow effect is limited—$40 million is marginal in ETH’s daily liquidity—but the second-order risk flagged by traders is behavioral contagion. If other ETH-heavy treasuries follow the playbook, selling the underlying to buy their own stock, the flow could become pro-cyclical: coins are sold to close equity discounts, the selling pressures spot, and wider discounts reappear as equity screens rerate to the weaker mark—repeat.

That is the “death spiral” scenario skeptics warn about when the treasury asset doubles as the company’s signal of conviction.